この記事では、スーパーアニュエーションや遺族年金について解説されています。遺族年金は国民年金や厚生年金保険に加入している遺族が死亡した場合に受け取れる年金で、遺族基礎年金と遺族厚生年金があります。配偶者が受け取れる遺族給付金の額や条件、計算方法、遺族給付金を受け取れない場合の対応についても詳しく説明されています。記事には中川義隆氏のアドバイスも含まれています。

When thinking about superannuation, many people associate it with a means of retirement funds for the future. However, in the event of the death of someone who was supporting a family, the surviving family members receive survivor benefits.

In this article, Mr. Yoshitaka Nakagawa of Clalas Tax Accountants will explain about survivor pensions based on his extensive knowledge and experience in tax and accounting services.

This article will provide a detailed explanation of the scenario where a husband passes away and the wife receives a pension.

Table of Contents:

What is a survivor pension?

How long can a spouse receive survivor benefits?

How is the amount of survivor benefits calculated for a spouse?

What happens if a spouse cannot receive survivor benefits?

Generalization

What is a Survivor Pension?

A survivor pension is the pension that surviving family members who are enrolled in the National Pension or Employees’ Pension Insurance can receive when the insured person passes away.

There are two types of survivor pensions: “Basic Survivor Pension” and “Employees’ Survivor Pension.” The wife of a deceased husband who is enrolled in the National Pension and meets the eligibility criteria can receive the Basic Survivor Pension.

Additionally, those enrolled in the Employees’ Pension Insurance and meet the qualifications can also receive the Employees’ Survivor Pension.

How Long Can a Spouse Receive Survivor Benefits?

Let’s explain how long a spouse can receive the above-mentioned Basic Survivor Pension and Employees’ Survivor Pension.

Basic Survivor Pension

This benefit can be received until the end of March of the year in which the child turns 18 or until the child reaches 20 years of age if they have a Level 1 or Level 2 disability. If the child grows up and exceeds this period, the payment period for the Basic Survivor Pension will end. However, if the surviving spouse remarries, they will no longer be eligible for the Basic Survivor Pension even if they have children.

Survivor Benefit Pension

When a husband passes away and there are children, or the wife is over 30 years old, the widow can start receiving the Pension for the Remaining Years from one month after the husband’s death. On the other hand, if the husband dies without children or if the wife is under 30 years old at the time of death, the widow can only receive the benefit for 5 years starting from the month of death.

How is the Amount of Survivor Benefits Calculated for a Spouse?

Now, let’s take a look at how much a spouse can actually receive in survivor benefits.

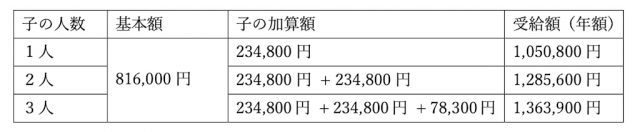

1: Basic Survivor Pension Amount (from April 2020)

The Basic Survivor Pension amount is calculated by adding the child allowance to the basic amount. The child allowance varies depending on the number of children. Here, children refer to those who have not yet reached the end of the year in which they turn 18 or under the age of 18. Those under 18 who qualify for disability pensions.

The basic amount and additional child allowance are as follows:

(1) Basic Amount

For those born on or after April 2, 1955: ¥816,000

For those born before April 1, 1955: ¥813,700

(2) Child Allowance

For the first and second child: ¥234,800 per child

Additional amount for the third child and later: ¥78,300 per child

The following table summarizes the benefits (annual) that a wife with 1-3 children (born after April 2, 1955) can receive.

Please note that if the wife has no children or if the children are over 18 (or over 20 in the case of a Level 1 or Level 2 disability), she will not be eligible for the Basic Survivor Pension.

2: Employees’ Survivor Pension Amount

The Employees’ Survivor Pension amount is 3/4 of the proportional part of the retirement pension amount of the deceased. The salary portion is determined based on factors such as the pension enrollment period and previous salaries.

The larger of the two amounts calculated using the following formulas is used as the proportional compensation component:

(1) Average Monthly Salary Basis (*1) × 7.125 / 1000 × 3 × Number of months as a member as of March 2003 + Average Standard Compensation Amount (*2) × 5.481 / 1000 × 3 × Number of months as a member after April 2003

(2) Average Standard Monthly Salary (*1) × 7.5 / 1000 * 3 × Number of months before April 2003 + Average Standard Compensation Amount * 2 × 5.769 / 1000 * 3 × Number of months after April 2003 × 1.041

When calculating the salary portion, if the enrollment period in the Employees’ Pension Insurance is less than 300 months (25 years), it is counted as 300 months.

If a person over 65 years old who is eligible for receiving old-age Employees’ Pension starts receiving the survivor Employees’ Pension due to their spouse’s death, an amount equivalent to “3/4 of the salary, proportional amount” is paid. The amount paid is the higher of half of the proportional salary part and half of their own pension, whichever is higher, up to the amount that the survivor paid.

Additionally, if the wife is between 40 and under 65 years old at the time of her husband’s death and does not have a dependent child or a child under 18 (or 20 in the case of a child), she will receive an additional ¥612,000 (annual) until she turns 65 along with the survivor Employees’ Pension (middle-aged and elderly widow allowance).

What Happens if a Spouse Cannot Receive Survivor Benefits?

If the wife’s children are independent or if she does not have children, she will not be eligible for survivor pensions. However, she may be eligible for widow’s pensions or lump-sum death benefits.

1: Widow’s Pension

A widow’s pension is paid to a wife who had been dependent on her husband until he turned 60 and had been married for more than 10 years, provided that the first primary insured person had paid National Pension insurance premiums for over 10 years before his death. The amount of the widow’s pension is 3/4 of the basic pension calculated based on the first insured period of the husband.

2: Immediate Gold at Death

A lump-sum payment is made when a person who paid insurance premiums for over 36 months as a primary insured person dies without receiving old-age basic pension or disability basic pension. The amount of the lump sum payment ranges from ¥120,000 to ¥320,000, depending on the number of months for which premiums were paid by the survivor.

In addition to widow’s pensions and lump-sum death benefits, if the husband’s death is considered a work-related accident (industrial accident), the survivor may be eligible for compensation under industrial accident insurance.

Generalization

In this article, we introduced an overview of survivor pensions and the amounts a wife can receive after her husband’s death. There are two types of survivor pensions: Basic Survivor Pension and Employees’ Survivor Pension. However, the period and amount of benefits differ, so it might be helpful to check how much survivor pensions you can receive.

●Contributions/Mr. Yoshitaka Nakagawa

Clalas National Tax Agency Executive Director, Tax Accountant

A tax consultant with wide-ranging experience in tax consulting, final tax return responses, organizational restructuring consulting, succession and business succession consulting, accounting outsourcing, and early settlement of a Tokyo Stock Exchange-listed company. Our policy is to provide advice on “smooth business succession” and “no discussion succession” tailored to each individual’s situation, and we have gained high praise and trust from many clients.

Clalas Japan Tax Accountants Corporation (

Composition and Editing/Keiko Matsuda (Kyoto Media Line/